[facebook][tweet][digg][stumble][Google][pinterest][follow id=”Username” size=”large” count=”true” ]

The President of the Federal Republic of Nigeria, Dr Goodluck Ebele Jonathan, through the Honourable Minister of Finance and Coordinating Minister of the Economy, Dr Ngozi Okonjo-Iweala eventually submitted the 2015 Federal Appropriation Bill to the National Assembly on December 17, 2014 – just a few days to Christmas and 14 days to the beginning of the new fiscal year. By this action, the government has once again laid the foundation for possible poor implementation of the 2015 budget, especially the capital component, considering that it may take up to six months before the Bill is enacted into law. Of interest then is when the government will learn to do the right thing by ensuring that the Appropriation Bill is enacted into law latest December 31 so that budget implementation can commence on January 1 in line with international best practice.

2014 Budget Performance

Even though the economy has experienced hiccups in 2014 as a result of the negative economic shocks from the global oil market and uncertainties in the global economy, the government is of the view that the economy is relatively strong, considering the estimated GDP growth rate of 6.34 percent, driven mainly by the non-oil sector. But as the oil sector which accounts for over 70 percent of government revenue and 96 percent of export earnings has been in trouble, how come the non-oil sector has apparently been doing so well in the face of unrelenting unconducive environment? This also leads to question marks on the single digit and declining rate of inflation put at 7.9 percent as at November, 2014 in the face of continuing liquidity surfeit propelled by continuous monetization of oil earnings. Even though US demand for Nigeria’s crude oil has virtually dried up, India and China are said to have come to the country’s rescue. Oil production has done fairly well at an average of 2.2 million barrels per day (mbd) compared to 2.38 mbd budgeted. The major shock then arose from declining oil prices from $114.0 per barrel last June to a little above $60.0 at present. Instability of prices and quantities are well-known features of the crude oil market. Wise countries overcome this by saving for the rainy day and managing such savings prudently. This has not been the case in Nigeria. Finally, on the 2014 budget implementation, the government has reported that recurrent budget releases were on track. This is understandable considering the nature of the expenditure items whose votes are easier to spend and squander by government officials. On the capital budget, N610.0 billion was said to have been released to the Ministries, Departments and Agencies (MDAs), most of which were cash-backed. This suggests 55.4 percent capital budget implementation. However, the rate of implementation is likely to be much lower, indeed, less than 50 percent, considering that not all the releases were cash-backed and not all the cash-backed amounts were spent because of the capacity problems of the MDAs and late enactment of the Appropriation Bill – 23rd of May 2014, leaving only about 6 months for capital budget implementation.

A Deflationary 2015 Budget

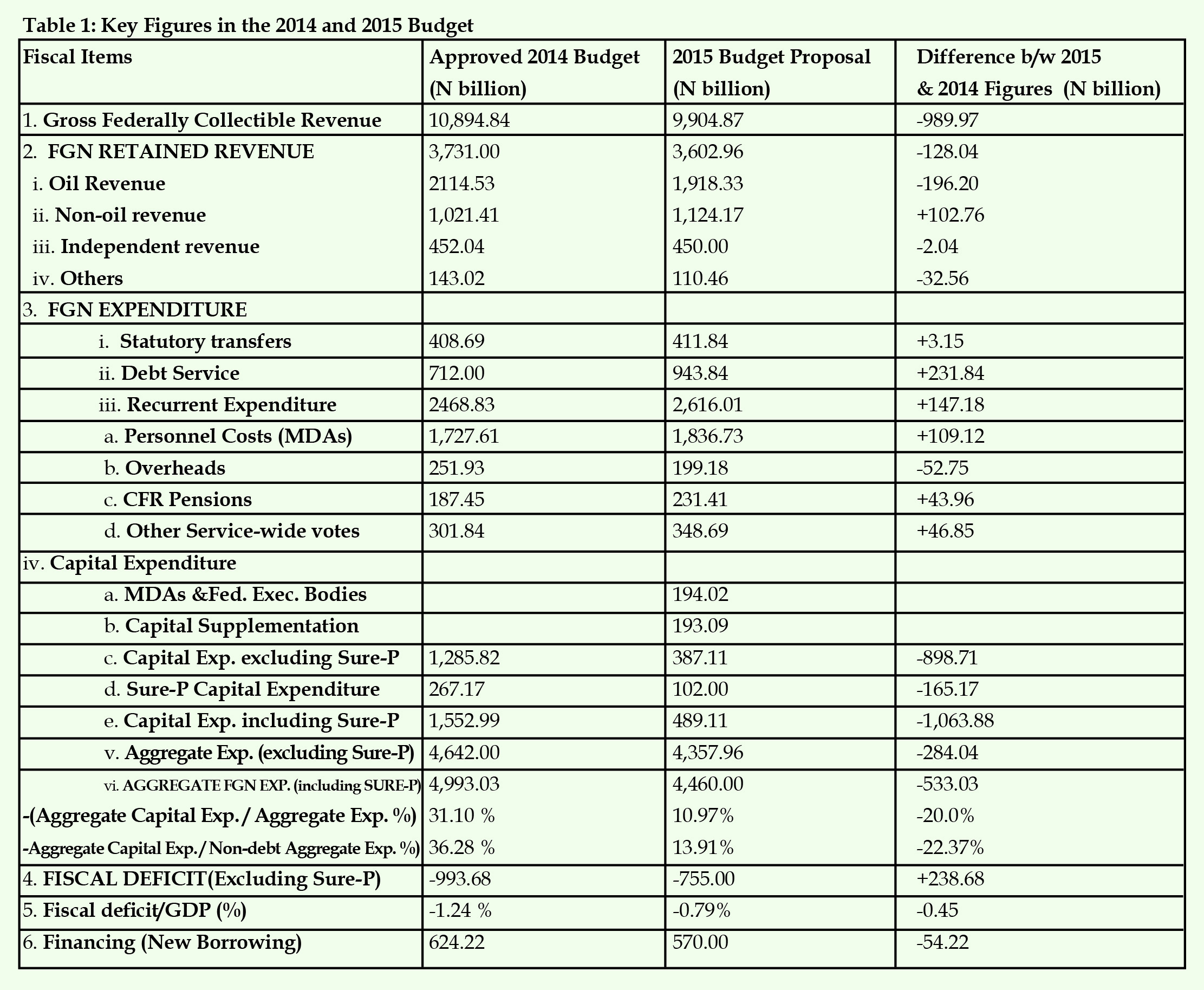

The proposed 2015 Federal budget is a deflationary budget, considering its size of N4,460.00 billion (including Sure-P budget) compared to the approved budget of N4,993.03 billion in 2014, a reduction by 12.0 per cent. This decline is very much higher than the 4.2 percent budget reduction in 2008. In all the other years (except 2004) since the democratic dispensation began in 1999, the annual federal budget has shown notable increases. Table 1 shows a comparison of the 2014 and 2015 budget figures.

The table implies a rather painful structural adjustment lying ahead. Because of uncertainties in the international economic environment, especially the oil market, oil revenue is projected to decline by N196.2 billion. Even though non-oil revenue is projected to increase, the Gross Federally Collectible Revenue, Federally Retained Revenue, Independent Revenue and Others are projected to decline by different magnitudes. In spite of this, all the recurrent expenditure items, except overhead, are projected to increase. It suggests the lack of political will to reduce the very high cost of governance, fuelled by the poor example in wages and salaries setting, duplication of government agencies and parastatals, among others. In contrast, the projected capital expenditure of N489.11 billion (including Sure-P) indicates a reduction by over N1.0 trillion in relation to the approved 2014 budget of N1,552.99 billion. The burden of adjustment is thus mostly borne by the capital budget, reflected in very low ratio of projected aggregate capital expenditure to aggregate expenditure of only 10.97 percent. The various MDAs bear the brunt of reduced capital budget in different degrees. And in terms of the total budget allocations, the government is upbeat that the priority sectors will be protected as much as possible. But with Defence and Security accounting for 28.03 percent (N985.79 bn) of aggregate non-debt expenditure, it is clear that priority has shifted from development expenditure to security that is challenged by the current insurgency in the country.

The deflationary nature of the budget is also reflected in and re-enforced by the key assumptions. The average oil production of 2.278 mbd may be realizable if the government achieves significant success in curbing the activities of oil pipeline vandals and thieves. But the benchmark oil price of $65.0 per barrel seems optimistic. The excess supply of oil in the world market is not likely to end soon. Demand has remained weak in the major oil consuming nations while OPEC has maintained a hardline position against reducing supply following its decision on the November 27, 2014. Politics appears to be gaining the upper hand over economics in the current oil market travails. The exchange rate of N168:$1.0 implies a devaluation of the naira by about 8.0 percent. Although this will have a positive effect on government revenue through the monetization of oil export earnings at the higher rate, the devaluation is at a great cost to the economy in terms of increase in the prices of goods and services, unemployment and poverty, among others. The pass-through effect of the exchange rate devaluation will be reflected in a higher rate of inflation in the country. And in an election year, the prospects of a single digit inflation rate being maintained are slim. Thus, against the backdrop of a deflationary budget, heightened inflation, and restrictive fiscal and monetary policies, the projected GDP growth rate of 5.5 percent is overly optimistic.

The Adjustment Measures

Now, the implications of the 2015 budget are such that most Nigerians may be in for a hard time, consequent upon the implementation of the adjustment measures proposed. They include scaling back of many intervention programmes and projects of the Federal Government through cuts in capital expenditure, fiscal measures which include surcharges on luxury goods and imported luxury items, review of tax waivers and exemptions, tightening of government spending through freezing of purchase of new equipment and other administrative capital, limit on international travel and training of public servants, and rationalization of expired committees and commissions. The adjustment measures, no doubt, have become inevitable, considering that reserves in the Excess Crude Account that could have been used to stabilize consumption have been squandered through wastes, inefficiency and corruption in public spending. But the measures do not go far enough. One desired area of fiscal adjustment is the drastic reduction of salaries and emoluments of government officials, elected representatives and other political office holders. The government must lead by example and cultivate the will to slash the emoluments of public office holders, top government officials and legislators. This action could discourage further agitations by different categories of public servants for salaries and wages increase. Also, the government should stop prevaricating on the recommendations of several committees/panels to rationalize the numerous parastatals and agencies of government which perform duplicated functions and have no evidence of value addition. As most of them are underpinned by law, the government should do the needful by sending the bills on the parastatals’ restructuring to the National Assembly for urgent action.

Overall, budget 2015 does not have much hope for many Nigerians. Rather, the implementation of the indicated structural adjustment measures will impact negatively on growth and welfare. In the handling of oil windfalls in the past, the spending behaviour of Nigerian rulers could be likened to that of a drunken sailor in a china wares’ shop. This must stop while inefficiency and corruption are eliminated from public spending. The government must develop a strong political will to maintain healthy Excess Crude Account and Sovereign Wealth Fund. These will enable the country in the future to prevent the type of painful adjustment measures envisaged in the 2015 budget occasioned by the absence of fiscal buffers to accommodate oil price and quantity shocks.

Mike Idi Obadan is a Professor of Economics at the University of Benin, Benin City

[divider]